Moving the stop to be safe

I am guilty of this for years. I move my stop to break-even to have a winner or 0 and not a losing trade. Especially if the move is significant, like 2-3R in my favor, it is difficult to chew a full -1R stop for me.

Recently, as I have been working on my trade bot written purely in DAS scripts, I came up with a trade management strategy of moving the stop to break-even after there is a 1R move. I am not going into the exact technical details, as this will be more of the mathematical part of the trade management.

The thing is, to be able to run the bot with any set of rules, I need to backtest the charts for all the possible entries, so I do that every day for a few weeks and have collected over 450 possible trade entries this year, complying with my entry criteria.

After filtering out different entry rules that give me a positive expectancy, here is what I ended up with.

What exactly is the “risk-free” trade for me?

I and my fellow trader @AimanBBT call this a risk-free trade because there is a high chance that the entry will not be retested because of the extension. In this strategy it is 143 (265-122) out of 265, or 54%.

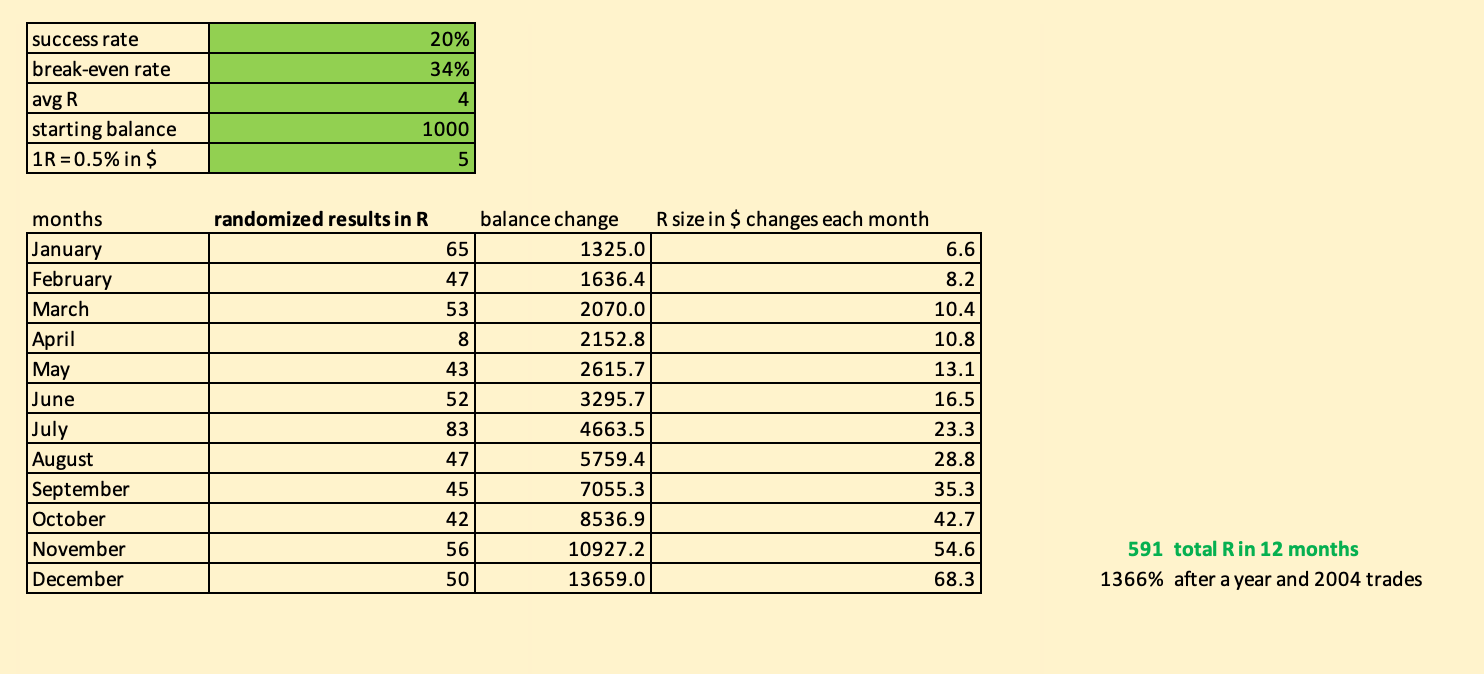

The risk-free stop trades are the ones where the trade moved 1R in my favor and got me out at break-even because of my moving stop trade management. My target is 4R, as it gives me the best totals. As you can see, the trading strategy has a positive expectancy that gives 90R of profits after 265 trades, or 0.33R per trade, because of the high winning R.

53 x 4 = 212R in winners

122 x -1 = -122R in losers

212 - 122 = 90 R in total profits because the 90 risk-free trades are 0.

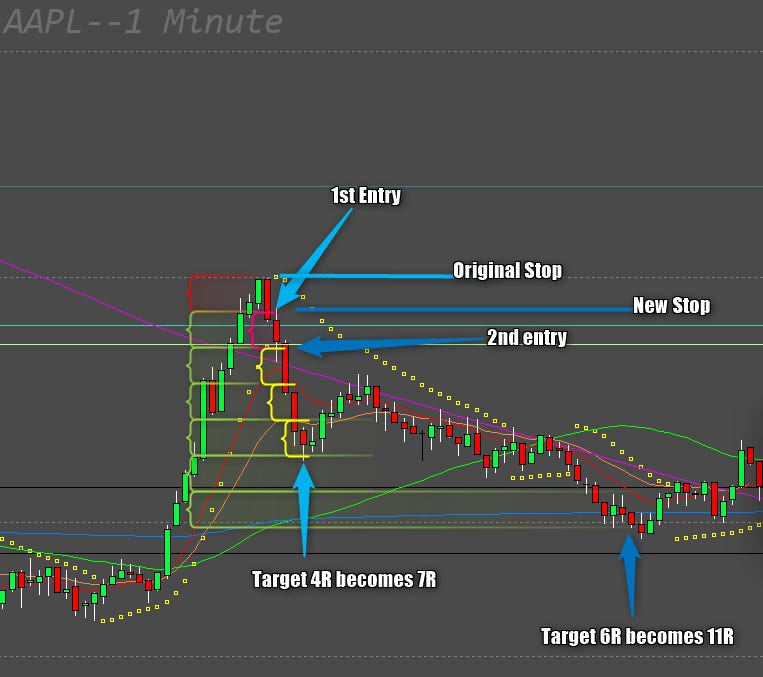

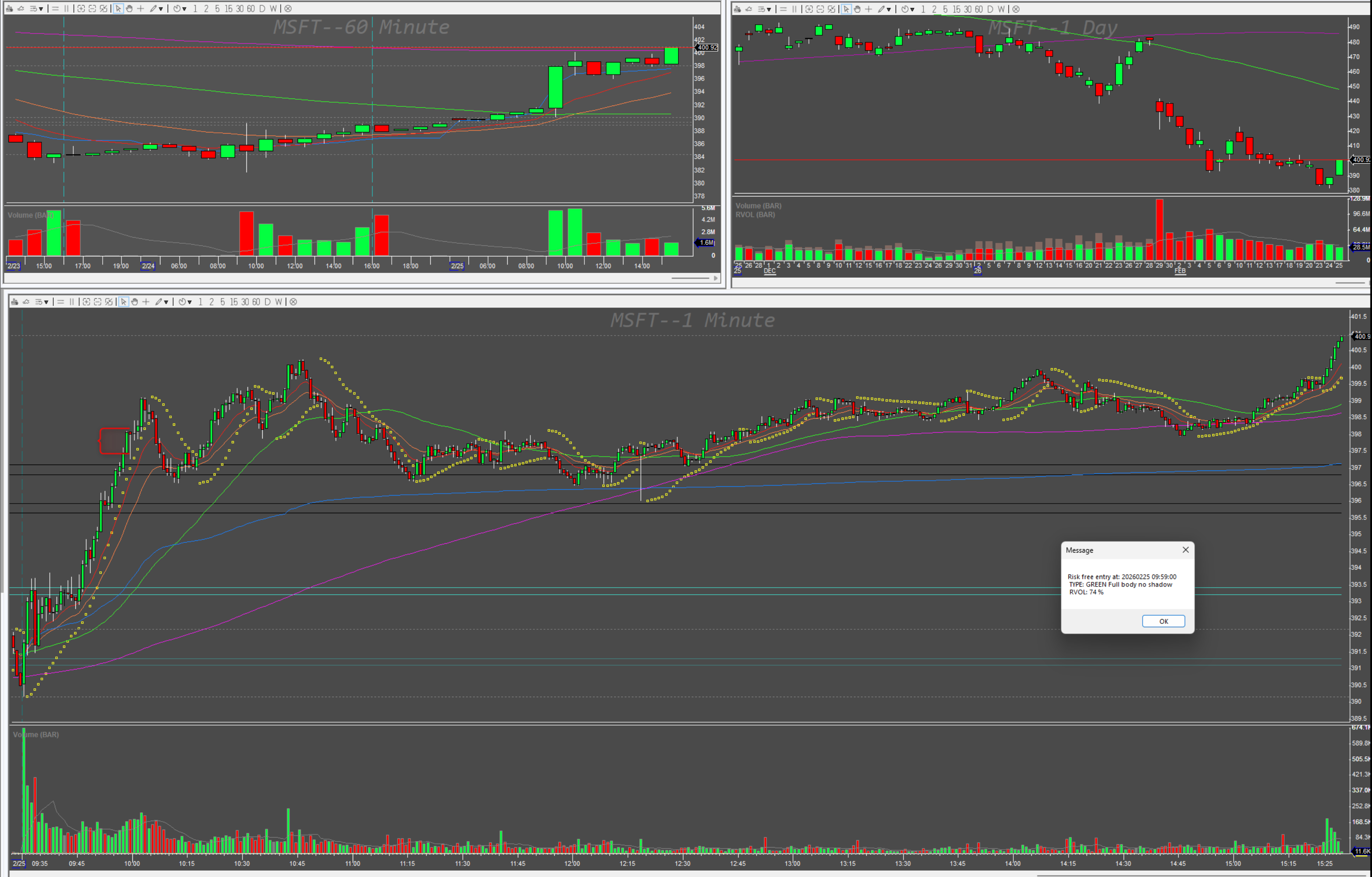

On a real chart, a stopped SHORT trade looks like this

It gives a 1R move after the entry, then the price action returns to the entry point, which means my trade ends with 0 profits.

On the other hand, a winning SHORT trade looks like this

It gives a 1R move, which is never retested, and continues towards my 4R target. With this strategy, it is the only scenario where I collect a winner.

This is where I realized that if it never retests the original entry, then maybe I can use the original entry as a new stop and risk 1R to get more if the target is reached.

Meaning, at 1R unrealized, I add 1R and target 3R on the new position. If I get stopped, I lose just the -1R from the new position and 0R from the first original position.

Why add and risk another 1R?

Remember the stats table

90 times I get stopped. That is -90R, but 53 times it never reached my original entry. So if the 2nd trade gives me 3R extra, that is

53 x 3 = 159R of profits

90 x -1 = -90R in losses

————————————-

+69R in total extra

That changes the table to

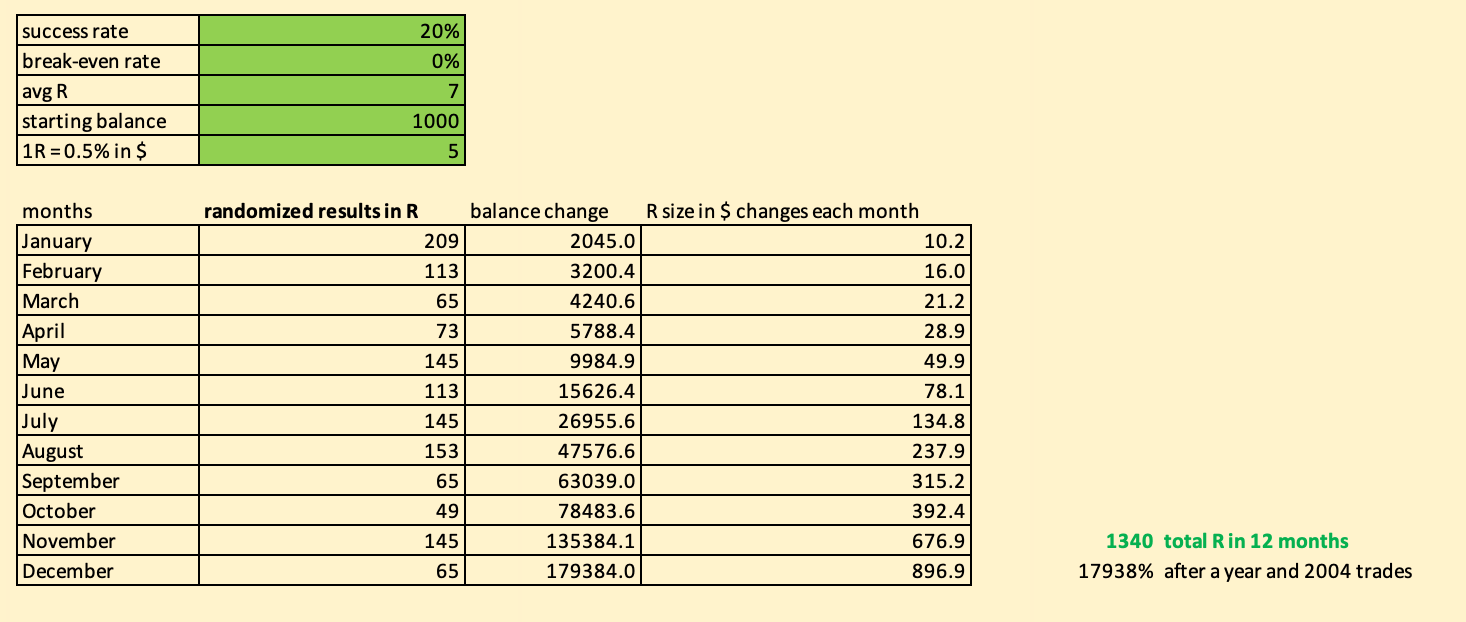

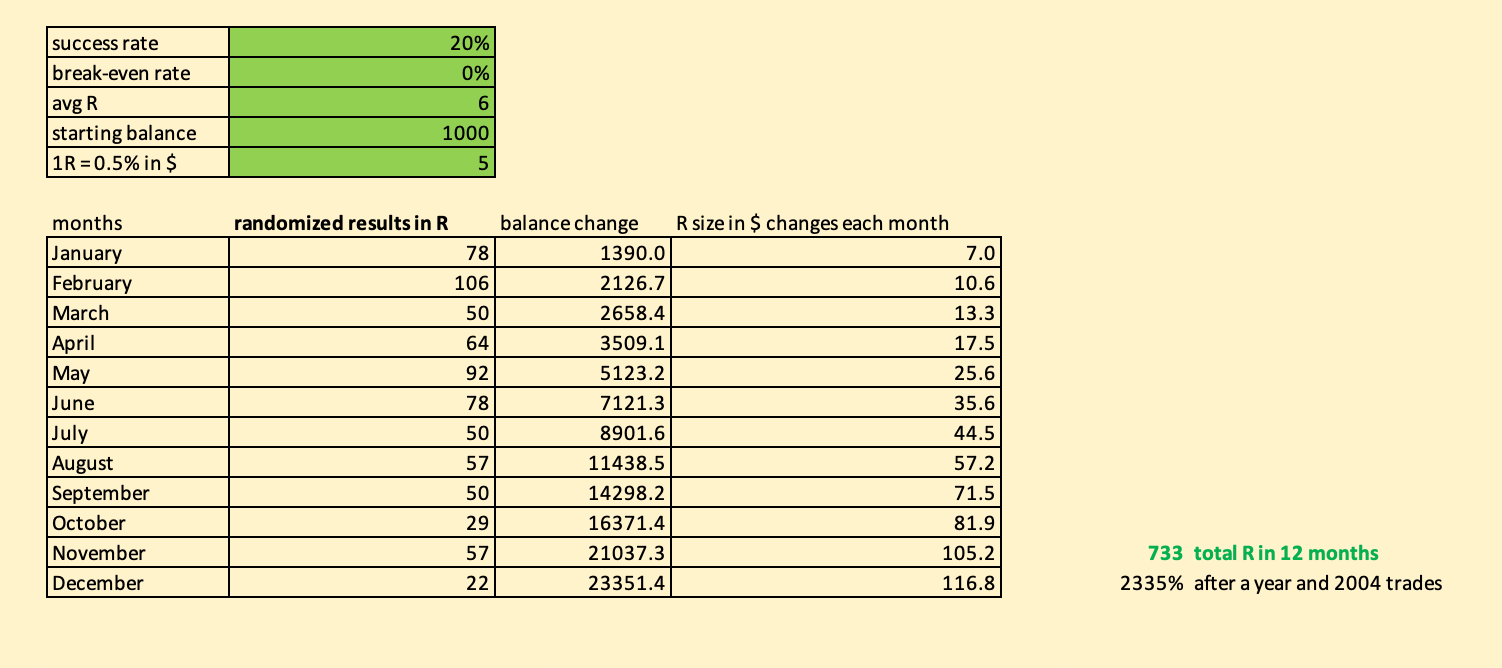

That is only a 20% win rate, but 7R in profits, and the number of trades is unchanged.

To count it even more easily, that is

20 winners of 140R and 80 losers of -80R per 100 trades.

Graphically it looks like this

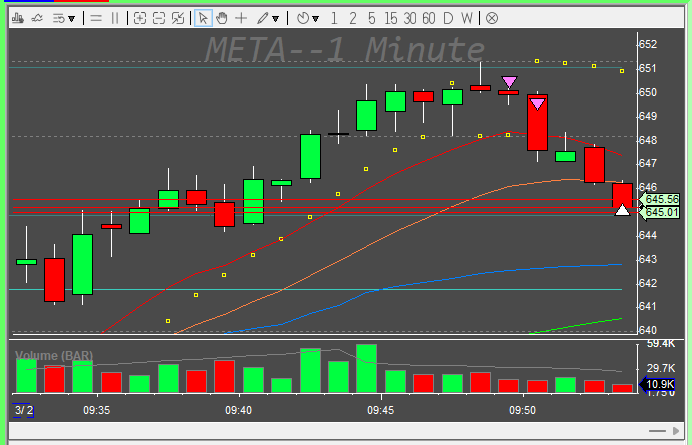

In real money trading, it looks like this

Enter, double the position, and exit.

I will lose more often too

Yes, from the 143 times doing it, I will lose 90 (expected outcome), which seems bad. But is it really that bad?

90 out of 143 is 63%

So for every 100 times my trade reaches 1R unrealized and I do the add-up instead of move stop to break-even, I get 37 x 3R and lose -63R.

That is +111R vs. -63R, giving me an +48R edge in my favor again.

Same trades, different management

Once you let the statistics work for you and avoid the mind tricking you with a wrong sense of safety, the results can surprise you.

It is still a 20% win rate, and even if I catch a slippage on each trade, even with a 6R average win, it is more profit at the end of the day simply because with the new trade management I am changing the chance of a loss slightly while the profit of a win gets disproportionately bigger.

In my previous post I showed the trade simulator (PM me if you want it, I am happy to share),

which gives me these numbers. Make sure to check it out.

Before, with the classic “move stop to break-even after 1R move” management

after the “add up” optimization in trade management

and counting in the slippage of 1R, giving just 6R average win it still beats the previous management

At the end it is quite similar to the parlay method I described here

How to find out gaps in trade management like this?

Surprisingly, not with AI, as many of the AI implementations of the trading journal software, including my preferred Tradersync just suck and give you just obvious advice and never do a real what-if scenario analysis.

I tried to upload my data to a few of the famous AI sites, but it failed. I admit it could be my ignorance and lack of skill, but I think that the fact that I did it myself at the end in a spreadsheet says it all.

It requires a very steady approach with either the trading itself (aka disciplined) or a backtesting mechanism. I have coded such a mechanism for my strategy in DAS Trader Pro, which I run every day, and it collects all the theoretical positions with automated screenshots like this for me.

No emotions, pure mathematical processing. Winners and losers, which I am able to quickly evaluate graphically as above.

You could do it using your own trade data using journaling software, but that will require a considerably longer time to collect, as this shows me trades that I could have taken if I was watching the chart at the time. The amount of data is crucial to confirm the statistical evidence.

Another crucial thing is to learn to fight the urge to be in the no-stress zone and do the statistically right thing instead of the mind calming thing.

Note that the above trade management is simple, and basically I could run a separate trade entry later on after the move to 1R unrealized has been confirmed, which will give me a bit different success rates and even better risk-to-reward ratios. Every idea like this takes hours and hours of digging in the data, so I might come up with something even more efficient later on.

I will describe the mechanisms in my backtesting in the future posts, so make sure you are subscribed to get notified on the new posts.

Thanks for the post Peter. What strategy or strategies are you using in your bot?